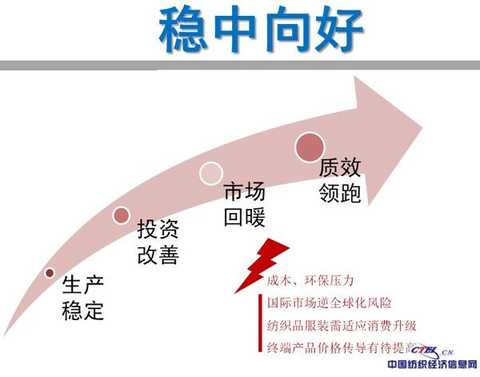

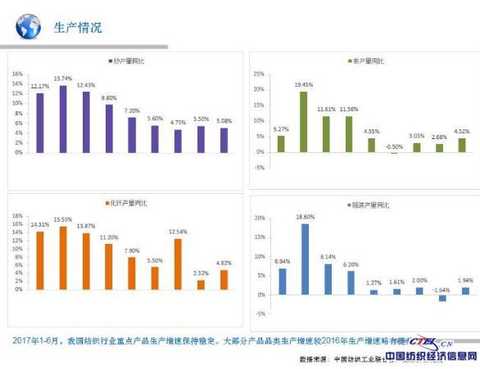

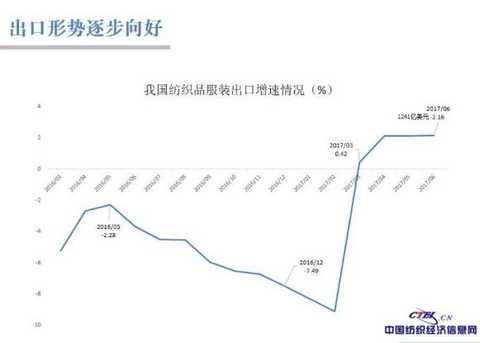

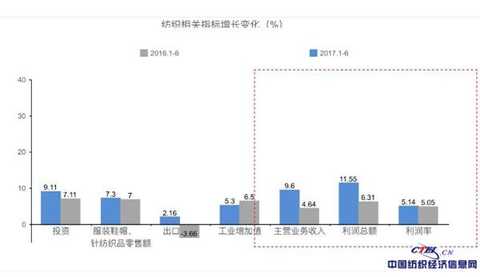

In the first half of 2017, in the face of the internal and external environment with high comprehensive cost and high international competitive pressure, the textile industry still insists on accelerating the transformation and upgrading, promoting intelligent manufacturing and green manufacturing, and cultivating new development momentum of the industry. With the steady advancement of the supply-side structural reforms, the effective implementation of the “three-product†strategy, under the circumstance of the country’s macro-stable optimism and sufficient momentum, the textile industry generally showed the characteristics of “stable and good, leading quality and efficiencyâ€. . In the first half of 2017, the main production indicators of the textile industry were flat. According to the National Bureau of Statistics, the output of chemical fiber, yarn, cloth and garments of enterprises above designated size increased by 4.8%, 5.1%, 4.5% and 1.9% respectively from January to June, maintaining a steady and small increase. From January to June 2017, the industrial added value of the textile industry increased by 5.3% year-on-year, which was 0.4 percentage points higher than the growth rate of industrial added value in 2016. Since 2017, it has shown signs of stabilization. The scale of investment continued to grow steadily. In the first half of the year, the completion of fixed assets investment projects of more than 5 million yuan in the textile industry was 613.01 billion yuan, a year-on-year increase of 9.1%. The growth rate was 2 percentage points higher than the same period of the previous year. It has gradually recovered since 2017. The regional layout adjustment continued to advance. The fixed assets investment in the eastern, central and western regions increased by 7.9%, 11% and 9.8% respectively from January to June. Except for the central region, the growth rate of investment increased by 8.8 percentage points over the same period of the previous year. In addition to the two-digit growth rate, the growth rate of investment in the eastern and western regions slowed by 1.2 and 21.6 percentage points respectively compared with the same period of last year. With the expansion of the base, Xinjiang's investment from January to June increased by 49.3% year-on-year. The growth rate has dropped from the same period of the previous year, but the contribution to the western investment has reached 150%. Since 2017, the textile industry's exports have stabilized and rebounded. According to China Customs Express data, in the first half of the year, China's cumulative exports of textiles and clothing reached US$124.05 billion, up 2.2% year-on-year. Since March, it has continued its negative growth for 22 consecutive months. Among them, the export value of textile yarns, fabrics and products was US$53.12 billion, up 3.1% year-on-year; the export value of clothing and clothing accessories was US$70.93 billion, up 1.4% year-on-year. From the perspective of major export enterprises, the total export value of private enterprises increased by 3.3% year-on-year, accounting for 67%, an increase of 1.8 percentage points over the same period of last year, and the endogenous power was stronger. The textile industry's exports have stabilized and the coordination has improved. From the perspective of market structure, the traditional markets of the United States, Japan and Europe are highly competitive. From January to May, China's share of the three major textile and apparel import markets in the United States, Japan and the European Union fell by 0.9, 1 and 0.5 percentage points respectively. In the same period, Vietnam's market share in the US, Japan and Europe increased by 0.8, 1 and 0.2 percentage points respectively. Bangladesh's market share in Europe increased by 0.4 percentage points year-on-year. Malaysia's market share in Japan and Europe increased. The textile industry in developed countries has accelerated the return and supply capacity, and the emerging countries in Southeast Asia have accelerated the layout of the textile industry and have significant cost advantages. They have put forward higher requirements for China's textile industry to maintain stable export competitiveness. The “Belt and Road†and emerging markets in Africa are flashing. In the first half of 2017, the textile industry exported a total of 42.91 billion US dollars of textiles and clothing to the countries along the “Belt and Roadâ€, accounting for 34.6% of China's total textile and apparel exports, an increase of 0.9 percentage points over the same period of the previous year. Among them, the export value of textiles and garments to Vietnam was 5.79 billion US dollars, accounting for 13.5%, which is China's largest export market for textiles and garments along the “Belt and Roadâ€. The export volume of textiles and clothing to Russia is 3.79 billion US dollars, accounting for 8.8%. Second only to Vietnam. From January to June, China's exports of textiles and clothing to Africa reached US$ 9.42 billion, a year-on-year increase of 4.1%, accounting for 7.4% of China's total textile and apparel exports, and roughly equivalent to Japan's textile and apparel exports. In the first half of 2017, thanks to the good performance of China's macro economy, the rebound in demand led to the growth of income and public expenditure of our residents, and continued to support the further improvement of residents' textile and apparel consumption. From January to June, the retail sales of clothing, shoes, hats and needles above designated size increased by 7.3% year-on-year, 0.3 percentage points higher than the same period of the previous year. The growth rate of online retail sales has accelerated. The nationwide online retail sales of online products increased by 20.8% year-on-year, 3.9 percentage points higher than the same period of the previous year, 5.2 percentage points faster than the first quarter, achieving the highest growth rate since 2016. The quality of operation has stabilized and the main business income and total profit have grown rapidly, becoming the “leader†of the main operating indicators of the whole industry. From January to June 2017, the textile enterprises above designated size achieved a revenue of 660.92 billion yuan, a year-on-year increase of 9.6%, and the growth rate was 5 percentage points higher than the same period of the previous year. The total profit reached 188.03 billion yuan, a year-on-year increase of 11.6%, and the growth rate was 5.3 percentage points higher than the same period of the previous year. The sales profit rate of textile enterprises above designated size was 5.1%, which was the same as that of the same period of last year; the turnover rate of finished products was 21.82 times/year, which was 5.4% higher than the same period of the previous year; the total asset turnover rate was 1.61 times/year, which was faster than the same period of the previous year. 2.7%; the ratio of three fees was 6%, a decrease of 0.1 percentage points from the same period of the previous year. In the first half of 2017, the textile industry continued its steady development trend and laid a solid foundation for the completion of the full-year target. Both the International Monetary Fund and the Asian Development Bank have raised China's annual economic growth forecast to 6.7%, affirming the positive prospects for China's stable economy. In the second half of the year, the global economic recovery is still continuing. China's economic rebalancing process has steadily advanced. The steady expansion of consumption, import and export, service industry and the steady recovery of private investment will all drive the continuous improvement of consumer confidence and the moderate growth of domestic and foreign market demand. However, the global trade uncertainty is increasing, the external development environment of the industry is complex and changeable, and the export competitiveness of the industry is still facing a big test. The textile raw material security needs to be strengthened and the comprehensive cost is high. The industry's own desire to accelerate transformation and upgrading is still urgent and remains stable. The good running pressure still exists. The textile industry will continue to adhere to the general tone of steady progress. Under the guidance of China's supply-side structural reform and innovation-driven development strategy, it will closely focus on the key tasks of the textile industry's 13th Five-Year Plan and the strategic goal of building a textile power. It also guides the important characteristics of household consumption upgrading, implements the “three products†strategy, accelerates brand building, and continuously consolidates the foundation of stability and stability. Strive to maintain a moderately stable cotton price, the industrial added value of the textile industry maintained a slight rebound in the year, the main business income and total profit increased steadily, and exports continued to show a stable and good trend, achieving the expected goal of full-year development. Editor in charge: Wang Zhen Bath Towel,Beach Towel,Microfiber Sports Towel,Sports Towel Changshu Aijia Knitting Products , https://www.microfiber-lovejoy.com