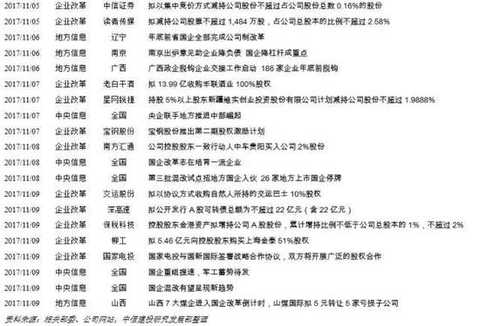

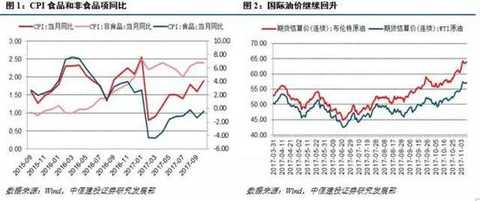

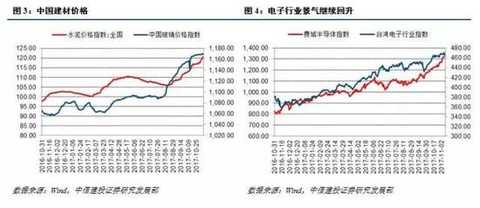

Ali employees earn Hong Kong stocks earn 10 million a year? Click here, you can also be the next TA! [Details] [CITIC Construction Investment Strategy Weekly] Expanding Openness and Embracing the World - Strategy Weekly Week 2 of November From WeChat public number: Jiantou strategy research Strategic week view In the second week of November 2017, the market continued to move up after a brief correction. The food and beverage sector and the financial sector, represented by liquor, led the market, and continued to rise in the semiconductor, communications and electronics sectors representing the future of China's new economic future. This confirms our investment strategy of “financial priority, value above, and growth in layout†in the fourth quarter. From the style point of view, the leading enterprises outperformed the small and medium-sized sectors under the support of industry concentration and performance, which is consistent with the long-term adherence to the style of “being beautiful and fat for beautyâ€. From the fourth quarter of 2017 to the first half of 2018, with the recovery of China's economy and the improvement of economic quality, the manufacturing industry represented by consumption upgrading and the new economy will be upgraded to become the main investment line for the whole year of next year. The Tang concept will continue in a style that is beautiful. China's expansion of capital market opening is another important milestone at this stage. Beginning on November 8, President Trump began his visit to Beijing, and China and the United States signed the largest order in history. With the recovery of the global economy, the trade level between China and the United States will reach new heights. This has an important supporting role for the economies and markets of China and the United States. On November 9, China announced that the financial industry will expand its opening to the outside world and lower the threshold for foreign investment in the banking, securities and insurance markets. The expansion of China's capital market has greatly supported the leading enterprises in the financial industry. We continue to be optimistic about the leading indicators in the big financial sector. In terms of the domestic economy, the CPI announced this week rebounded slightly to 1.9%, and the PPI remained at a high level of 6.9%. This reflects the process of a moderate recovery in the Chinese economy. Among them, the rebound of food items helped the CPI to rise more than expected, but the inflation rebound was still moderate, and the PPI was flat year-on-year, mainly due to the strong support of consumer goods and processing industries. From the perspective of the industry, the situation in the Middle East, OPEC production cuts and other factors are still the potential driving force for the upward movement of oil prices. The building materials boom in the middle reaches continues to rise, while the price of waste paper falls and the price of paper products rises high or improves the profitability of downstream paper enterprises. The downstream electronics and liquor boom better. Therefore, in terms of industry configuration, we still insist on recommending the food and beverage sector and home appliances sector that CPI will benefit from. From a policy perspective, monetary policy remains tight. IPO audits are tightening and liquidity remains relatively stable next week. As the disturbance factor is less in the next week, the stacking expiration volume is significantly reduced. The central bank's open market operation has become a core variable affecting liquidity. It is expected that the “peak cutting and valley filling†operation will continue, and the liquidity will fluctuate between 2.8% and 3.0% next week. Monetary policy continues to remain relatively stable. From the perspective of investment strategy, China's expansion of the capital market's opening to the outside world has become the main line of change in this phase and in the future. The financial sector, especially leading financial companies, will continue to benefit. We are firmly optimistic about the market from 4Q to 2018 in 2017, continue to grasp the main line of the food and beverage and home appliance sectors brought about by the consumption upgrade, continue to grasp the new economic main line driving China's future development, and be optimistic about industries such as semiconductor, communication and intelligent manufacturing. In terms of style, the market will still follow the value of “big beauty, fat beautyâ€. 1 Domestic economy: inflation has rebounded moderately, focusing on the middle and lower reaches of the economy The food item helped CPI to go up, and the PPI was flat and resilience. In October 2017, the CPI was 0.1%, up 1.9% year-on-year, and the increase was higher than last month. The PPI rose 0.7% from the previous month and rose 6.9% year-on-year. In terms of structure, the year-on-year growth rate of CPI was mainly driven by food items; while PPI was flat year-on-year, mainly due to the strong support of consumer goods and processing industries. With the rebound of the base in December and December, the superposition of pork and vegetable prices is weak, and inflationary pressure is expected to be limited. From the upstream, coal consumption of power generation is still low, the price of thermal coal rebounds, industrial metal is mostly adjusted back, and oil prices continue to rise. As of November 9, the coal consumption of power generation of the six major power plants rebounded by 7.92% compared with the previous week, but it was still at a low level. The price of thermal coal futures rebounded sharply by 3.98%, but the spot price of Qinang Q5500 fell by 2.88%. Iron ore 1801 rebounded 4.42%. LME3 industrial metal prices mostly rebound, but lead rebounded slightly, nickel, zinc, aluminum prices are still relatively strong. Recently, oil prices continued to rise. IPE oil and WTI crude oil (continuous contract) futures rose 2.29% and 2.10%, respectively, to close at 63.49 US dollars / barrel and 56.81 US dollars / barrel. From the midstream, the building materials continued to boom, steel prices fluctuated at a high level, chemical chlor-alkali and PTA prices went up, and paper prices remained high. China's cement and glass price index rebounded for 11 consecutive weeks and 13 weeks, respectively, up 3.83% and 1.08% from the previous week. Rebar HRB400 and hot rolled coil Q345 rose 2.03% and 1.18%, respectively. Jianying Chemical's prosperity index fell, pesticides and fertilizers were still booming, the transaction price of glyphosate reached 28,000/ton, the price of urea producer was 1,770 yuan/ton, and the ex-factory price of phosphoric acid was 4,950 yuan/ton. In addition, the price of chlor-alkali and PTA rose. The domestic market price of waste paper continued to decline. The domestic distribution price of softwood pulp rose slightly by 0.4%, the price of paper products was flat, and the prices of copper and double-adhesive papers rose. From the downstream, the land transaction in the third-tier cities rebounded. In October, the auto market was selling well, the electronic boom continued to rise, and pork and vegetable prices were weak. As of November 5, the transaction area of ​​the main 100 cities has rebounded, and the transaction area of ​​the third-tier cities has continued to rise. According to the data of the association, the retail market in the passenger car market in October was strong (sales of 64,600 units per month), and wholesale sales were positive (monthly sales of 66,600 units). Electronic boom is still picking up, the Philadelphia Semiconductor Index and Taiwan's electronics industry index rose 1.63% and fell 0.54%. This week, the BDI index has fallen back. In terms of liquor, the price of No. 1 shop Feitian Maotai (53 degrees) and Wuliangye (52 degrees) was 1,299 yuan / bottle and 989 yuan / bottle, respectively, the high level. The wholesale price index of agricultural products fell by 0.43% from the previous month, and the performance of pig prices and vegetable prices remained weak. Opening to the outside world: China's financial opening Trump visits China On November 8, US President Trump arrived in Beijing to start a visit to China. Two days before Trump's visit to China, the amount of trade orders signed by China and the United States reached US$253.5 billion. China and the United States have cooperated in various fields such as energy and chemical industry, agricultural products, aircraft manufacturing, life sciences, and smart cities. Trump's visit to China became an important step for China to promote opening up after the 19th National Congress. Judging from the overall situation of China's foreign trade, with the recovery of the global economy, China's import and export volume has shown an upward trend since 2016, and has gone out of the process of gradual downward trend since the financial crisis. From the perspective of trade balance, China's trade balance growth rate is close to zero, which shows that China has begun to move toward a trade balance and gradually began to show the characteristics of a mature economy. As the most important foreign trade partner of China, the United States has shown a similar trend to the US import and export volume. China's foreign financial industry is open On November 9, China announced a substantial relaxation of the financial access system and expanded the level of opening up of the financial industry at its own pace, including market access for the banking, securities fund and insurance industries. The opening of the financial industry is an important step in expanding the opening up to the outside world and an important milestone in the integration of China's capital market into the global capital market. On November 10, Vice Minister of Finance Zhu Guangyao said at the briefing of the State Council Office that China has decided to relax the investment ratio limit of direct or indirect investment in securities, fund management and futures companies by single or multiple foreign investors to 51%. After three years of implementation of the above measures, the investment ratio will be unrestricted; the foreign-funded banks and financial asset management companies will be eliminated from the single-shareholding of foreign-funded banks by no more than 20%, and the total shareholding ratio will not exceed 25%. The proportion rule of the equity investment in banking industry; after three years, the investment ratio of insurance companies that have invested in the establishment of personal insurance business by single or multiple foreign investors will be relaxed to 51%, and the investment ratio will not be restricted after five years. For the industry, companies with earlier international business layouts will benefit first, and the financial industry's style of “being beautiful and fat is beautiful†will continue to strengthen. From the perspective of the banking industry, Bank of China and Industrial and Commercial Bank will benefit first; leading brokers in the securities industry will benefit first, such as Guotai Junan and CITIC Securities; comprehensive large insurance companies in the insurance industry will continue to benefit. From the perspective of investment strategy, Sino-US economic and trade exchanges continue to heat up, which will support the economies of both countries. China has expanded its degree of opening up to the outside world, raised the level of opening up, and played a supporting role in the growth of the financial industry. Leading companies in the financial sector will continue to benefit. From the perspective of the global market, the Hong Kong market will benefit from the economic recovery and trade between China and the United States and will be further supported. 3 Policy perspective: IPO audits are tightening, and liquidity is stable next week IPO review is tightening, central bank adjusts car loan policy It is expected that the tightening of the IPO review will be a continuing trend in the future, and the supervision and maintenance of the healthy development of the capital market will be strengthened. On November 7th, only one of the six listed companies in the meeting had “customs clearanceâ€, and the other five were rejected. The pre-review rate was only 16.7%. According to statistics, since the 17th National Development and Reform Commission took office after the National Day holiday, a total of 36 start-up companies will be reviewed and 20 will be successfully passed. The attendance rate is only 56%. Strict IPO audits prevent enterprises from “listing for diseaseâ€, which is a key part of financial comprehensive supervision. It is also the general direction set by the fifth national financial work conference in July this year. It is expected to be an important trend for future sustainability. In the context of IPO acceleration, the review of strictness is conducive to improving the quality of listed companies and maintaining the sustainable and healthy development of the capital market. Strengthen supervision over mergers and acquisitions, and speculation is the focus of supervision and prevention. On November 9th, Gu Bin, the executive manager of the Shanghai Stock Exchange, said at the 3rd China M&A Summit Forum, “There are some problems in the process of mergers and acquisitions. These issues are also some of the issues that the SFC has been trying to regulate and contain over the years. Bad factors." The negative factors referred to in this area mainly concern the four major problems of overvaluation, speculation, interest transfer and market value management. M&A supervision is still the direction established since the Fifth National Financial Work Conference. Focus. The central bank and the China Banking Regulatory Commission adjusted the car loan policy, implemented the adjustment of the economic structure, and promoted the development of the green environmental protection industry. On November 8, the People's Bank of China and the China Banking Regulatory Commission adjusted the auto loan policy in accordance with the “Guiding Opinions of the Banking Regulatory Commission of the People's Bank of China on Increasing Financial Support for New Consumption Sectorsâ€. Since January 1, 2018, the self-use of new energy vehicle loans has been the highest. The distribution rate is 85%. This is an important measure for the CBRC to implement the State Council's policy of adjusting the economic structure and release the diversified consumption potential. It has far-reaching significance for promoting the economic development of the green environmental protection industry and improving the quality and efficiency of the automobile consumer credit market. Financial de-leverage has seen initial results, and liquidity is relatively stable next week. This week, liquidity continued to be more relaxed, and it is judged that it will remain relatively stable next week. Since November is neither a tax-paying big month nor a fiscal expenditure big month, the issue of superimposed local bond issuance is limited, and liquidity disturbance factors are few. The central bank's open market operation is the most central variable affecting liquidity. From the indicators such as M2 growth rate and leverage ratio, it can be judged that the current financial de-leverage has achieved staged results. The monetary policy will continue to maintain a stable neutrality and timely fine-tune the hedging. It is judged that DR007 will fluctuate between 2.8%-3.0% next week. Sex will remain relatively stable. This week, the central bank began to withdraw funds, continue to "cut the peak", and net return of 310 billion yuan. As of November 10 this week, the net return of 310 billion yuan. Specifically, this week, the central bank resumed a net return on Monday, Tuesday and Wednesday. The net withdrawals were 1,600,800, and 40 billion yuan. On Thursday, the company returned to zero and stabilized. On Friday, the net return was 30 billion yuan. This week, from Tuesday to Thursday, the 63-day variety reverse repurchase will continue to be launched. The central bank continues to fine-tune the liquidity and protect the funds at the end of the year with obvious intentions. The current financial de-leverage has initially achieved results, and monetary policy remains unsettled. The fine-tuning of monetary policy “cutting peaks and filling the valley†will continue. This week, the overall liquidity continued to be more relaxed, with most interest rates going first. From the perspective of interest rate trends, DR007 went up this week, with an average weekly interest rate of 2.9073%, up 10.35BP from the previous quarter. This week, most of the SHIBOR went up and went up. Overnight, 1W, 1M and 3M interest rates rose 13.41 BP, 1.40 BP, -0.25 BP and 2.74 BP respectively this week. If you do not consider the central bank's open market operations next week, the liquidity gap next week is about 262.5 billion yuan, significantly lower than this week. Next week's liquidity is analyzed from the perspective of the central bank's open market operations and fiscal deposits. (1) The open market operation due amount next week is 422.5 billion yuan, lower than this week. As of November 9th, next week, the central bank’s public operation reversed repurchase maturity amounted to 422.5 billion yuan (reverse repurchase maturity of 300 billion yuan, MLF due amount of 122.5 billion yuan), compared to this Weekly open market operation dues are down by RMB 267.5 billion. (2) The fiscal deposits in November are expected to decrease by nearly 624.9 billion, with an average of about 160 billion yuan per week. In the past five years, the average monthly fiscal deposits were 597.2 billion, while the average fiscal deposits in November were -2.77 billion, a decrease of about 622.9 billion yuan compared with October, and an average weekly reduction of nearly 160 billion. . (3) The remaining amount of local bond issuance is limited, which is good for funds. In the first three quarters of this year, new local government bonds were issued at 1.4 trillion yuan, and the annual issuance quota was 1.63 trillion yuan (local fiscal deficit of 830 billion yuan, local special bonds of 800 billion yuan). 4 Market Review This week, the market for SSE (1.31%), Shenzhen Stock Exchange (2.31%) and entrepreneurship (1.98%) rose across the board. In the industry, 24/29 industries have risen. Electronic components, communications, home appliances, computers, and national defense military have become the main force driving the rise. Only construction, real estate, and transportation have continued to decline. In the secondary industry, industries such as black goods, semiconductors, telecommunications operations, electronic equipment, communication equipment manufacturing, and computer hardware are among the top gainers. In terms of topics, the board index, 360 concept index, 3D sensor index, chip localization index, Quantum communication index, 3D printing index, wireless charging index, IPV6 index, and OLED index rose by a large margin, ranking first. In the context of liquidity neutrality, the support of economic fundamentals is an important basis for current small and medium-cap stocks and cyclical growth. At the current time, the cyclical correction reflects certain concerns about the fundamentals of the economy, so the market switches to the defense sector such as consumption and finance. Another support for traditional consumption is current expectations of performance, but when traditional consumption peaks in the short-term profit growth of real estate peaks, the market will begin to seek new possibilities. We believe that the emerging industries including tmt are firstly affected by the upstream price fluctuations, and the new direction is the new momentum of future development. In the fourth quarter, emerging industries will ushered in valuation restructuring and lead new value. In the long run, we insist on performance as the key link and continue to be optimistic about the support of the downstream sector. At the current time, focus on investment opportunities for valuation switching. From the perspective of configuration, the industry is concerned with the media, medicine, liquor, and finance. On the theme, focus on emerging manufacturing, military-civilian integration, beautiful China, and Beijing-Tianjin-Hebei integration. 5 Industry configuration: performance as the key, preferred financial consumption Industry Focus: Finance, Consumption bank: The bank's ability to sustain healthy development is guaranteed and investment risks are reduced. First of all, the quality of listed banks continued to improve this year. The total non-performing loans decreased by 8.98% year-on-year. The weighted average of non-performing loans decreased by 8 bp. The overall provision coverage ratio was 6.91 percentage points higher than the end of last year. Moreover, under strong supervision, the scale of bank asset expansion has slowed down, reducing the risk of performance fluctuations. At the same time, after the restructuring of the debt structure, the overall interest rate stabilized and rebounded, and continued profitability improved, improving performance expectations. Brokerage: In October, the Shanghai Composite Index successfully broke through 3,400 points, and the balance of the two companies quickly broke through the trillion mark. The stock market confidence was boosted. It is expected that the trading enthusiasm will continue and provide effective support for the brokerage performance. And the current brokerage PB is mostly between 1.4X-1.6X, the valuation has fallen sharply, and the average dividend rate of the brokerage sector is over 30%, and still has value investment opportunities. medicine: Since the beginning of the year, the world's major pharmaceutical sectors have shown differentiation. The Hang Seng Mainland China Health Care Index outperformed the market by more than 7%, ranking first in the world. China's A-share medical index rose but underperformed the broader market. From the perspective of valuation, driven by the continuous introduction and innovation of heavy products, the net profit growth rate enjoys a certain premium, and the valuation of A-share pharmaceutical white horse stocks is still within a reasonable range. Liquor: This year, the performance of the liquor industry generally exceeded expectations, and the market style was self-reinforcing. The market remained optimistic about the performance of the 18-year liquor industry, so the liquor industry valuation reached a high level. If the current market style maintains a structural market, the current stock price will be digested and adjusted in the short term, and the market will continue. The liquor stocks are worthy of attention. Performance expectation: changes in earnings forecasts for the past two weeks and January Judging from the changes in industry earnings forecasts in the past two weeks, non-bank financial, steel, construction materials, light industry manufacturing, transportation and other industries are forecasting higher earnings forecasts, communications, defense and military, textile and apparel, automotive, media, agriculture, forestry and animal husbandry. Profit forecasts for industries such as fishing fell more. From the data of the past month, the profit forecast of steel, food and beverage, non-silver finance, building materials, non-ferrous metals and other industries is among the highest, communication, computer, textile and garment, electrical equipment, national defense military, medical biology, electronics, Earnings forecasts for agriculture, forestry, animal husbandry and fishery, machinery and equipment, light industry manufacturing, and automobiles have declined. From the PB valuation, the current valuation of moisture below 50% of the industry includes mining (26%), chemicals (43%), architectural decoration (41%), electrical equipment (33%), mechanical equipment (44%) ), national defense military (37%), textile and clothing (45%), commercial trade (31%), agriculture, forestry, animal husbandry and fishery (%), leisure services (43%), public utilities (49%), real estate (30%), Computer (44%), media (31%), banks (26%), non-bank financial (38%), comprehensive (32%); the current A-share overall valuation is slightly lower than the average, of which, the main board, small and medium-sized board and The valuation of GEM is 41%, 49% and 48% respectively. From the CITIC style index, the cycle and growth are still higher than the average, and the financial, consumption, and stability are lower than the average. 6 topic tracking Xiong'an New District: Alibaba officially entered the game to promote comprehensive cooperation On November 8, Alibaba Group signed a strategic cooperation agreement with Hebei Xiong'an New District Management Committee. At the same time, Alibaba also announced that the three subsidiaries have completed registration in Xiong'an, namely Alibaba Xiong'an Technology Co., Ltd., Ant Jinshun Xiong'an Digital Technology Co., Ltd. and Cao Ying Xiong'an Network Technology Co., Ltd., which is Alibaba's entry into Xiong'an. A landmark step, Alibaba will cooperate with Xiong'an New District in the fields of cloud computing, big data, smart logistics, inclusive finance and e-commerce to help Xiong'an New District become the future of mobile smart city. "model room". Ma Yun said: "Alibaba's starting point is not to go to Xiong'an to do business, but to come up with the most advanced technical strength and innovative resources to make Xiong'an New District a benchmark for the future city and a sample of China. Every week, Xiong An will launch at least one policy information related to Xiong'an New District. Examining the current information, the most microscopic is the establishment of the Xiong'an Group. Just as the government's official definition of the company: Xiong'an Group is the main carrier and operation platform for the development and construction of Xiong'an New District in Hebei. Its main functions are to innovate investment and financing mode, introduce social capital through multiple channels, carry out PPP project cooperation, raise funds for new district construction, build a new district investment and financing system; carry out land first-level development, affordable housing and commercial real estate development and construction; Baiyangdian environmental comprehensive rectification and tourism resources development and management; responsible for the new district transportation and energy infrastructure, municipal public facilities construction and franchise; participate in the development and construction of various parks and major industrial projects in the new district. We are looking for relevant investment directions to study key companies involved in PPP, real estate, environmental protection, tourism, transportation, energy, and utilities in the Beijing-Tianjin-Hebei region. Environmental protection: Trump visits China to sign a large order, focusing on energy and environmental protection Environmentally friendly new energy is a new chapter in Sino-US cooperation. From November 8th, US President Trump visited China. During his visit to China, the United States will conduct commercial negotiations with some Chinese companies. The total amount of signed projects for two days will exceed US$250 billion, creating a historical record covering the construction of the Belt and Road. , energy, environmental protection, chemical, cultural, pharmaceutical, infrastructure and other fields. Among all the contracts, energy, especially the new energy cooperation project, has the largest amount. On November 9, the National Energy Investment Group and the US West Virginia announced the signing of a framework agreement to invest in the latter's shale gas, power and chemical production projects. At $33.7 billion, the Alaska government, Alaska Gas Development Corporation, Sinopec, and China Investment Corporation signed an agreement with Bank of China to promote LNG development in Alaska. China is currently stepping up environmental governance and urgently need to adjust its energy structure. The many cooperations between China and the United States in the fields of energy and environmental protection are of positive significance for improving the proportion of clean energy and ensuring China's energy security. State-owned enterprise reform At the central level , on Friday, the front page of the study time published the article signed by Hao Peng, secretary of the Party Committee of the State-owned Assets Supervision and Administration Commission, demanding that the building of a socialist modernization power be a cohesive force, and that the state-owned enterprises should "propose a good team for a great struggle and build a great project." To be a pioneer, to build an important foundation for the advancement of a great cause, and to build a first-class enterprise for the realization of a great dream." On Tuesday, the People’s Daily published a paper stating that the central enterprises have joined forces to promote the rise of the central region, combine the advantages of central enterprises with local resources, and promote the rise of the local economy. On Thursday, China Securities Journal issued a document, and the reform of state-owned enterprises is expected to present a new trend. In the future, it is likely that state-owned assets will not pursue absolute control, attach importance to strategic cooperation with new partners and increase the proportion of core employees. From the dynamics of the central level this week, with the continuous deepening of reforms, the third batch of mixed reform pilots recruited local state-owned enterprises, and the market-oriented mixed ownership reform is accelerating. Based on the new requirements of the 19th National Congress for state-owned enterprises, state-owned enterprises will continue to promote reforms in areas such as maintaining and increasing state-owned assets, strengthening state-owned capital, and preventing the loss of state-owned assets. At the local level , the provincial state-owned enterprises in Liaoning Province completed the reform of the company system before the end of the year. The transfer of government and enterprise decoupling enterprises in Guangxi Province of Guangxi Province started 186 enterprises before the end of the year. Nanjing City issued opinions to help enterprises reduce debts and reduce the leverage of state-owned enterprises into the key points of the seven major coal enterprises in Shanxi Province, Shanxi Province, entering the countdown to state-owned enterprises reform. Shanmei International plans to transfer 5 loss-making subsidiaries to 5 yuan. The reform of state-owned enterprises in various localities has been frequent, the basic layout has been continuously optimized, the quality and efficiency have increased steadily, and the vitality of state-owned enterprises has been continuously enhanced. At the enterprise level , AVIC High-Tech Unit Tokyo National Development Fund plans to reduce its holdings of 31.1 million shares, accounting for 2.23% of the total share capital. Xining Special Steel intends to sell its four subsidiaries under the controlling shareholding of the East Iron and Steel Group, with a 100% stake in all but 70%. Reader Media intends to reduce the company's stock by no more than 14.84 million shares, accounting for no more than 2.58% of the company's total share capital. Baosteel Co., Ltd. launched the second equity incentive plan. Laobai Dry Wine is planning to acquire a 100% stake in Fenglian Wine Industry for 1.399 billion. From the perspective of enterprise dynamics, the restructuring and merger of state-owned enterprise assets is an important measure to promote the reform of mixed ownership. Local enterprises have actively responded to the call for reform of the state's mixed ownership system, and corporate reform has continued to deepen. In terms of investment proposals , the 19th National Congress focused on building a “world-class enterprise with global competitivenessâ€, and this part will also be built around state-owned enterprises. Therefore, in the future, the reform of state-owned enterprises, especially the mergers and acquisitions of central enterprises (reducing competition in the same industry, creating upstream and downstream integrated enterprises, upgrading the industrial structure), and the reform of mixed ownership (introducing private capital and expanding the control of state-owned capital) remain the focus. Military industry: military-civilian integration and state-owned enterprise reform are the direction In the report of the 19th National Congress of the Communist Party of China, in the "New Era Thoughts and Basic Strategies of Socialism with Chinese Characteristics", it is clearly stated that "more emphasis will be placed on military-civilian integration"; and "strong military with Chinese characteristics" is also a key issue alone in the ten Discussed in the Nine Reports. It is worth noting that the phased objectives of military industry are the same as the time cuts for building a well-off society in an all-round way. This also reflects the characteristics of the same fate of military industry and the national economy, and also implies that military industry will usher in long-term high-speed growth opportunities. Investment suggestion: It is recommended to pay attention to the concept of military-civilian integration and state-owned enterprise reform: the preferred national team leader (especially the CATIC system, the degree of marketization is high, the listed company's core assets account for a high proportion, the most benefit from the release of the industry chain performance); Minsheng Military Company (higher technical threshold, large market space, core competitiveness and first-mover advantage, reasonable valuation); can also pay attention to the phased opportunities brought about by mixed reform: mainly the small market value of South Ship, Weapon, and Aerospace the company. Sina statement: This news is reproduced from the Sina cooperation media, Sina.com posted this article for the purpose of transmitting more information, does not mean agree with its views or confirm its description. Article content is for reference only and does not constitute investment advice. Investors operate on this basis at their own risk. Enter [Sina Finance and Economics Unit] Discussion Ladies Tops,Lady Chiffon Top,V Neck Ladies Tops,Long Sleeve Blouse Woman Top Shaoxing Moonten Trade Co., Ltd , https://www.moontenshirts.com

2

2

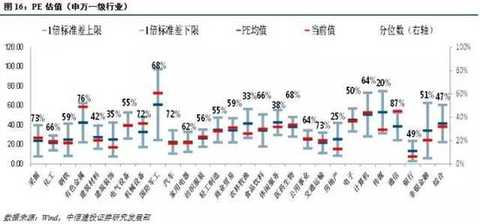

Valuation situation

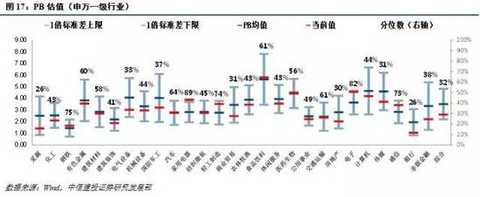

Valuation situation